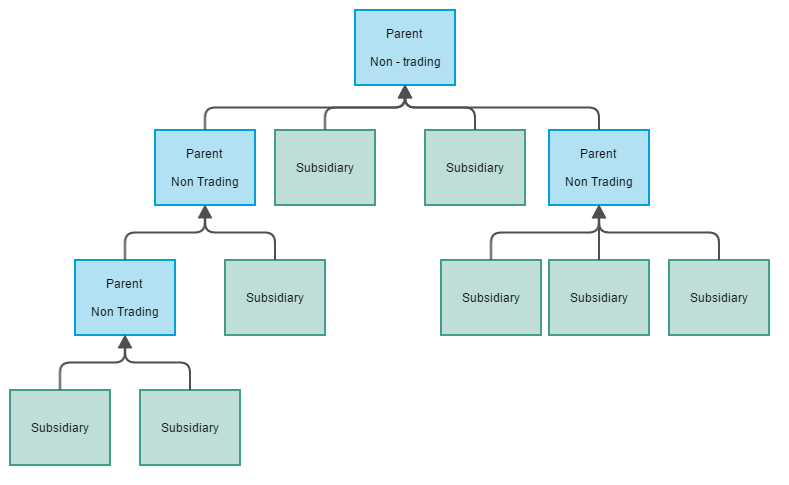

If your organisation is made up of several subsidiary companies, you can use consolidation in Sage 200 to produce management reports at the parent company level.

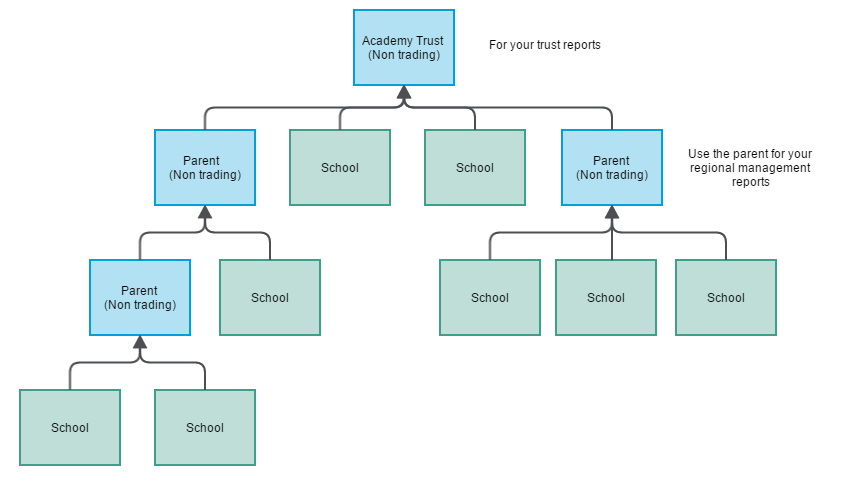

If you're a multi academy trust, you can use consolidation in Sage 200 to create reports at trust level, such as the SOFA report, that include the required financial information for all the schools within the trust.

How it works

- The consolidation is run from each subsidiary

- Each nominal account (Code, CC and Dept) in the subsidiary

- The balance of all nominal accounts, at the end of a selected period, is transferred from each subsidiary to the parent

- The balance of each nominal account in the subsidiary is posted to the linked nominal account in the parent

- The value of the consolidation transaction is the difference between the actual trial balance in the subsidiary, at the end of the selected period, and the trial balance the last time the consolidation was run.

Requirements

-

The parent

- The parent and all subsidiaries must have the same base currency.

-

The parent and all subsidiaries should all have the same chart of accounts.

This includes the same cost centre, department,

-

The parent and subsidiaries should have the same accounting periods.

Note - warningNominal account balances are passed to the parent by accounting period. If the accounting periods are different in the parent and subsidiary companies, this could lead to discrepancies in the your financial reports.

-

If the only consolidated report that you need to run from your parent

Just consolidating the balances once a year makes errors less likely.

This is because:

- All transactions should be posted to the correct accounts in your subsidiaries by the end of the year.

- It'll be easier to check that any new nominal accounts that have been added to a subsidiary

- If mistakes are made, you only need to correct them for one period rather than 12.

Consolidating to more than one parent

When consolidating, the parent should only be used for reporting purposes. If you want to consolidate to more than one parent, then you'll need a Sage 200 company for each parent.

What do you want to do?

Sage is providing this article for organisations to use for general guidance. Sage works hard to ensure the information is correct at the time of publication and strives to keep all supplied information up-to-date and accurate, but makes no representations or warranties of any kind—express or implied—about the ongoing accuracy, reliability, suitability, or completeness of the information provided.

The information contained within this article is not intended to be a substitute for professional advice. Sage assumes no responsibility for any action taken on the basis of the article. Any reliance you place on the information contained within the article is at your own risk. In using the article, you agree that Sage is not liable for any loss or damage whatsoever, including without limitation, any direct, indirect, consequential or incidental loss or damage, arising out of, or in connection with, the use of this information.